AUGUST 2025 – Farmers, construction contractors, and non-road equipment manufacturers are navigating a turbulent economy marked by tight margins, weak demand, and high borrowing costs. Yet, industry experts say that while the short term looks difficult, the long-term outlook appears increasingly bright.

“In the short and medium terms, the economic environment remains very challenging,” said Al Melhim, AEM’s senior director of business intelligence, during AEM’s “Business Intelligence Q3 Equipment Market Outlook” webinar on Aug. 7. “High interest rates, falling commodity prices, and rising inventories are still exerting downward pressure on AEM’s three key sectors. These conditions have led to tighter margins, cautious capital investment, and slower equipment turnover. Additionally, policy-related headwinds such as high tariffs and labor shortages have continued to strain operational efficiency and workforce availability.”

Despite the hurdles, Melhim sees conditions improving in the years ahead.

“We see a shift toward positive momentum as a result of The One Big Beautiful Bill Act (OBBBA) framework,” Melhim said. Beneficial provisions include tax incentives, extended farm support, biofuel and rural energy incentives, and infrastructure spending—all of which could serve as economic catalysts for agriculture and construction.

The OBBBA’s incentives are expected to gradually ease capital pressures on farmers and contractors, while also spurring investment in infrastructure and clean energy projects that ripple through equipment markets.

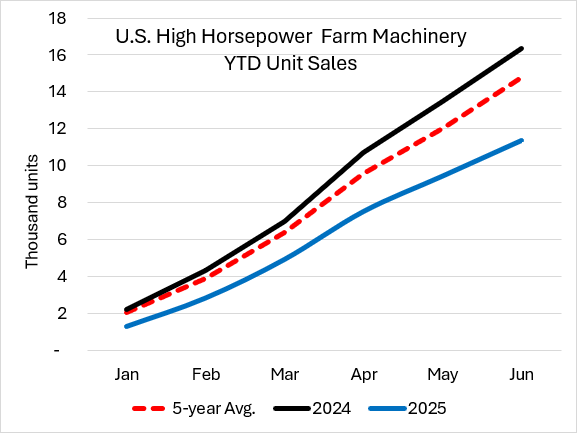

The ag sector is still feeling the pinch:

One potential boost comes from accelerated depreciation rules, which make larger and more expensive machinery more attractive investments for farmers. Still, Melhim noted that “the elevated interest rates have increased borrowing expenses, making it harder for farmers to justify large capital investments in new machinery.”

Auction prices are climbing, aligning more closely with asking prices. This trend often signals a coming shift to higher demand for new equipment, as buyers lose leverage in the used market.

Yet the financing environment continues to weigh heavily. Financed new equipment sales have dropped at a CAGR of 11% over the past year, while financed used equipment sales fell 7%. “It’s a heavy weight that continues to linger on the industry,” Melhim said.

Globally, construction is expected to grow 2.27% in 2025, down from earlier forecasts of 2.8%. Growth is expected to rebound to 3.3% in 2026, and average nearly 3.75% annually from 2027–2029.

In the U.S., construction output is forecasted to grow 1.02% in 2025, down sharply from earlier expectations of 4%. Growth is then projected at 1.4% in 2026 and around 2% annually from 2027–2029.

Notably, the forecasts do not yet include potential benefits from the OBBBA, which could give a lift to the Industrial and Energy & Utilities sectors. Residential construction is also projected to rebound through the end of the decade.

However, rising construction material costs remain a major drag:

For now, uncertainty remains. Foreign direct investment in North America has slowed sharply, with capital expenditures in U.S. FDI projects dropping 16% in Q1 and 36% in Q2 of this year.

Still, as Melhim emphasized, the long-term trajectory points upward. With federal policy providing incentives, global demand stabilizing, and infrastructure spending ramping up, both agriculture and construction may be on the cusp of stronger growth after a difficult stretch.

Originally reported by Association of Equipment Manufacturers.