The global repaintable anti-graffiti building facade coatings market is projected to grow from USD 310.0 million in 2026 to approximately USD 598.5 million by 2036, expanding at a compound annual growth rate of 6.8%, according to new market forecasts.

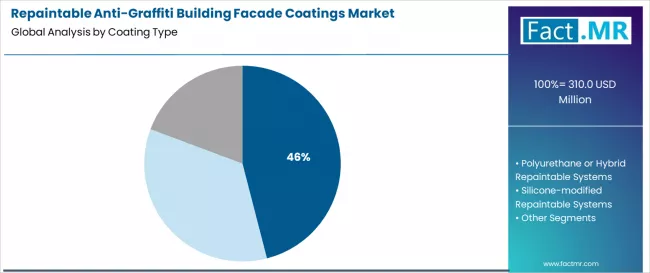

Water-borne acrylic repaintable systems are expected to dominate the market, accounting for about 46% of total demand, driven by their low VOC content, ease of application, and strong adhesion to mineral substrates. Concrete and masonry facades represent the largest surface substrate segment, holding a 52% share, reflecting the widespread use of these materials across urban commercial, institutional, and residential buildings.

Professional contractor application remains the preferred deployment method, representing roughly 63% of installations. Market analysts note that proper surface preparation and controlled application are critical to ensuring coating durability, cleaning-cycle resistance, and long-term performance.

Demand for repaintable anti-graffiti coatings continues to rise as municipalities and property owners seek cost-effective solutions to protect building facades from vandalism without repeated recoating or surface damage. Innovations in hybrid and silicone-modified chemistries are further enhancing durability, weather resistance, and aesthetic preservation.

The repaintable anti-graffiti building facade coatings market is poised for sustained global expansion over the next decade, fueled by rising urbanization, increasing graffiti vandalism, and growing investment in long-term building maintenance strategies. Market forecasts indicate the sector will nearly double in value, growing from USD 310.00 million in 2026 to USD 598.51 million by 2036 at a CAGR of 6.8%.

Among coating technologies, water-borne acrylic repaintable systems are projected to maintain leadership with a 46% market share. Their dominance is attributed to environmental compliance, strong adhesion to porous substrates, ease of cleaning, and the ability to withstand multiple graffiti removal cycles without compromising facade appearance. These characteristics make them a preferred choice for public buildings, commercial properties, and transportation infrastructure.

Concrete and masonry facades represent the largest addressable surface area, capturing 52% of market demand. These materials are widely used in urban construction and are particularly susceptible to deep graffiti penetration, creating consistent demand for protective, non-porous coating systems that preserve both aesthetics and structural integrity.

Professional contractor application accounts for approximately 63% of the market, reflecting the technical precision required for correct installation. Industry stakeholders emphasize that performance outcomes depend heavily on surface preparation, application thickness, and substrate compatibility, making trained contractors essential for warranty compliance and long-term effectiveness.

Key market drivers include the high cost of repeated graffiti removal, regulatory requirements to maintain clean urban environments, and increased awareness of total cost of ownership among municipalities and property owners. At the same time, challenges remain, including higher upfront costs compared to conventional paints, performance limitations in extreme climates, and the need for better education around cleaning protocols.

Geographically, growth is strongest in developed markets with dense urban centers. The UK leads with a projected CAGR of 7.2%, supported by urban regeneration initiatives and heritage preservation mandates. Germany follows at 6.8%, driven by stringent maintenance standards and advanced coating innovation. The United States is forecast to grow at 6.5%, supported by large commercial real estate inventories and active municipal graffiti abatement programs, while Japan’s 5.9% growth reflects high urban density and rapid adoption of advanced material technologies.

Competition in the market includes major architectural coatings manufacturers and specialized protective coating providers. Companies such as Akzo Nobel N.V., PPG Industries Inc., Sherwin-Williams, RPM International, Hempel, and KEIM Mineral Coatings are competing through performance guarantees, integrated system solutions, and expanded technical support for specifiers and contractors.

As cities increasingly prioritize facade preservation, sustainability, and long-term asset protection, repaintable anti-graffiti coatings are expected to become a standard component of both new construction and refurbishment projects worldwide.

Originally reported by Fact MR.