Strong absorption across 83% of markets points to renewed confidence as development pipeline finds equilibrium

The U.S. industrial construction sector is showing clear signs of bottoming out after years of dramatic decline, according to Newmark's latest fourth quarter market report. With the development pipeline stabilizing at 282 million square feet—the lowest level since 2018—the industry appears to be finding a sustainable balance between supply and demand.

"The U.S. industrial sector is confidently building momentum. 83% of U.S. industrial markets recorded positive absorption in Q4, a vast improvement from 50% during Q2's peak uncertainty. The worst is definitely behind us, and we're moving toward consistent, broad-based stabilization," said Lisa DeNight, Head of North American Industrial Research at Newmark.

After plummeting 59% year-over-year in Q2 2024, construction starts have moderated their decline significantly. Fourth quarter 2025 starts were down just 7% compared to the prior year, with the pipeline actually growing by a few million square feet in Q3 before declining again in Q4. This fluctuation suggests the market has reached an inflection point where new development is beginning to align more closely with actual tenant demand.

Quarterly construction starts totaled 65.6 million square feet in Q4 2025, while the total construction pipeline stood at 282.9 million square feet—down 12.8% year-over-year but showing signs of stabilization after consecutive quarters of sharp contractions.

Despite improved market dynamics, construction costs continue to challenge developers. The Producer Price Index for new warehouse construction stands at 238—more than double pre-pandemic levels. While tariffs have kept costs elevated following inflation-driven increases, the market has largely stabilized as developers leverage current conditions to negotiate better pricing.

The sustained high costs are reshaping development economics. Projects must command higher rents to pencil, which has naturally limited speculative construction and contributed to the pipeline contraction. However, this dynamic is also creating a quality gap in the market, as older facilities struggle to compete with modern logistics requirements.

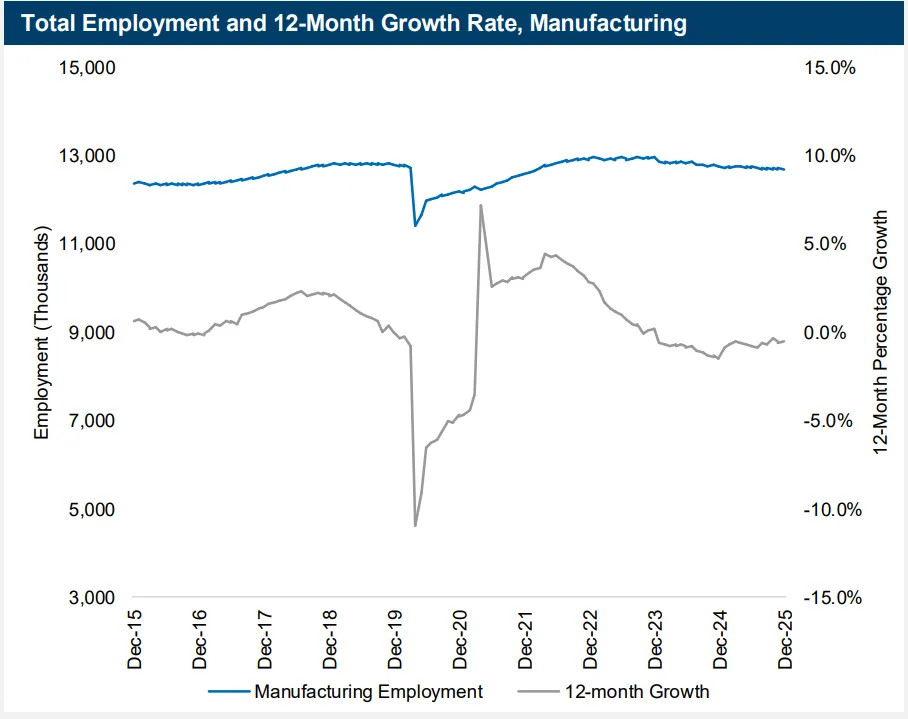

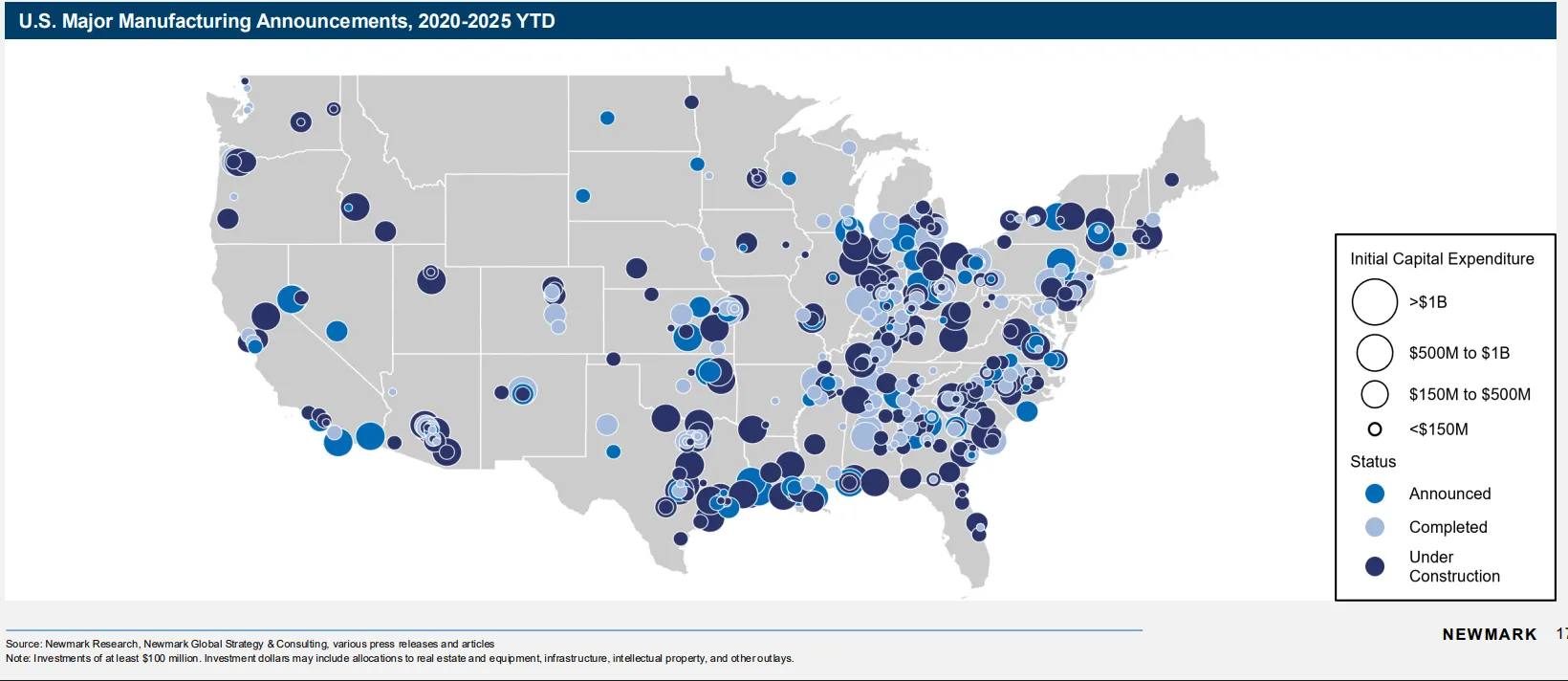

A major bright spot for industrial construction comes from domestic manufacturing expansion. Since 2020, approximately $772 billion in manufacturing investments have been pledged across the U.S., supporting over 400,000 new jobs and a minimum of 350 million square feet of new industrial projects. Much of this development has already been delivered.

Four sectors are driving the greatest investment volumes: high-tech and digitalization, automotive and transportation, energy, and biomanufacturing. These advanced manufacturing facilities require purpose-built spaces with specifications far beyond traditional warehouse construction, creating opportunities for specialized developers.

The broader leasing market delivered its strongest net absorption in two years during Q4 2025, with just over 60 million square feet absorbed—nearly matching the approximately 70 million square feet in new deliveries. Total 2025 absorption reached 150.9 million square feet, up from cyclical lows but still the softest annual total since 2012.

New leasing activity remained robust at 911.1 million square feet for the year, up 6.2% year-over-year, with particular strength in larger box-size segments. Flight-to-quality trends continued to propel Class A properties to capture a growing share of new leasing activity.

The national vacancy rate stood at 7.5% in Q4 2025, up 64 basis points year-over-year. While vacancy is expected to see incremental increases before stabilizing mid-year 2026, the pace of increase has slowed dramatically. Market observers note there's more upside than downside risk to the outlook, with vacancy potentially peaking earlier than conservative forecasts suggest.

The investment sales market also showed renewed vitality, with transaction volume up 12% compared to 2024. Fourth quarter sales activity was the strongest since 2022, with sequential increases each quarter throughout the year. Total 2025 sales volume reached $104 billion, with particular strength in newer, larger building transactions.

Cap rates have held steady in the mid-5% range over the past 12 months, with average top-quartile industrial properties trading at 5.5% and average total industrial cap rates at 5.9%. Meanwhile, public market cap rates have compressed nearly 100 basis points since April, suggesting private market cap rates may follow suit in coming quarters.

With elevated availability and flat rents creating optimal conditions for tenants to upgrade space, a wave of lease expiries is expected to drive continued absorption. For construction firms and developers, the key challenge will be identifying markets where tightening fundamentals justify new projects at current cost levels.

The industry's pivot toward quality and the ongoing nearshoring trend should continue supporting demand for modern facilities, particularly in markets with strong logistics infrastructure and access to manufacturing corridors. As economic uncertainty moderates and the construction pipeline stabilizes, the sector appears positioned for a measured recovery rather than another development boom.

Sourced from Newark 4Q25 US Industrial Market - Conditions & Trends