The pace of construction cost growth moderated during the first quarter of 2026, but ongoing investment in data centers, advanced manufacturing facilities, and infrastructure projects continues to shape pricing and procurement conditions across the U.S. construction market.

According to the latest quarterly construction cost analysis from Mortenson, nonresidential construction costs rose 1.69% during the first three months of the year, while annual cost growth reached 6.77%. Although escalation remains a concern for owners and contractors, the report suggests market conditions have become more stable compared with the volatility experienced in recent years.

Demand for steel, copper, aluminum, and other metal-intensive materials remains elevated as large-scale industrial and technology projects move forward. Tariffs, geopolitical uncertainty, and energy-related cost pressures continue to influence pricing for many construction inputs, particularly those tied to electrical infrastructure and specialized building systems.

Data centers and advanced manufacturing facilities remain among the most influential drivers of construction activity nationwide. These projects are increasing competition for skilled labor, fabrication capacity, and critical equipment in several regions.

While overall labor availability has improved relative to previous years, localized shortages remain a challenge in specialized trades and electrical work. Procurement concerns also persist, particularly for long-lead power distribution equipment and other components required to support energy-intensive facilities.

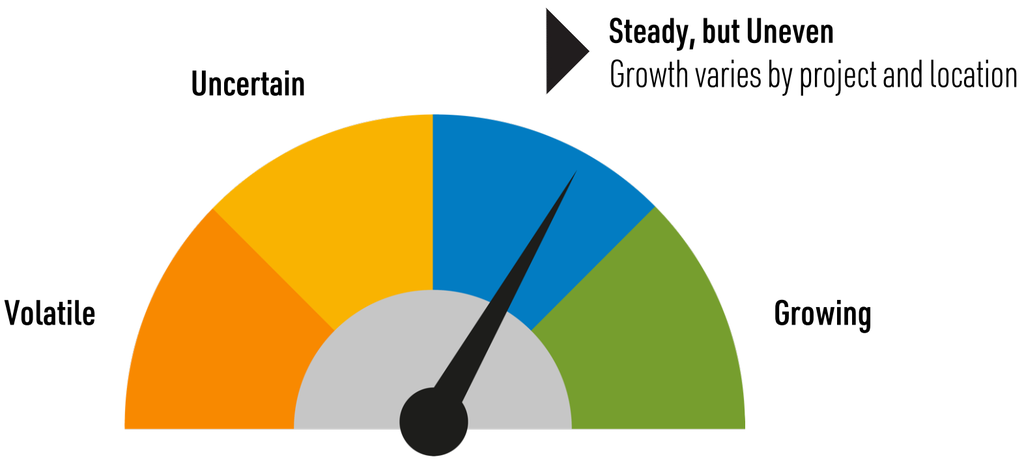

The report found that project activity varies significantly by region. Markets benefiting from large industrial developments continue to experience stronger demand and tighter labor conditions, while some commercial and institutional sectors are seeing more competitive bidding environments as contractors pursue a smaller pool of traditional work.

Construction material costs continued to rise during the quarter, with metal-related scopes experiencing some of the largest increases. Structural steel, metal decking, fabricated stair systems, plumbing materials, and fire protection components all recorded notable cost growth.

Transportation and logistics networks have largely stabilized compared with the disruptions of previous years, helping improve supply chain reliability. However, trucking expenses and international freight costs remain elevated due to fuel prices, operating cost inflation, and ongoing geopolitical challenges affecting global trade routes.

For project owners, these conditions reinforce the importance of early procurement planning and supply chain coordination, especially for projects with significant electrical, mechanical, or structural steel requirements.

Despite ongoing cost pressures, several leading indicators point to stronger construction activity heading into the second quarter of 2026.

Construction starts increased 13% in March, supported by continued investment in nonresidential sectors. Planning activity also remains robust in areas such as healthcare, energy, infrastructure, manufacturing, and data center development.

In addition, architectural billing activity has shown signs of improvement, suggesting a healthier project pipeline could emerge later in the year. Industry observers view these indicators as evidence that owners and developers remain willing to advance projects despite economic uncertainty and elevated construction costs.

For construction owners and developers, the current market presents a mix of opportunities and challenges. Cost escalation has become more predictable, but project budgets remain vulnerable to fluctuations in metals, electrical infrastructure, and energy-related materials.

At the same time, strengthening project pipelines and rising construction starts indicate continued confidence in long-term capital investment. Owners that engage contractors early, secure critical equipment ahead of schedule, and maintain flexible procurement strategies may be better positioned to manage risk as demand grows in key sectors.

As the industry moves further into 2026, project outcomes are increasingly being shaped by market-specific conditions, making regional labor availability, material sourcing strategies, and procurement timing critical components of successful project delivery.

Source: Mortenson Construction.